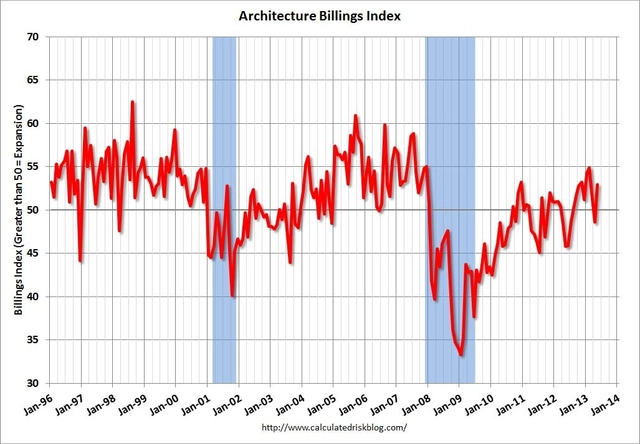

The Architecture Billings Index (ABI) remained positive again in June after the first decline in ten months in April. As a leading economic indicator of construction activity, the ABI reflects the approximate nine to twelve month lag time between architecture billings and construction spending. The American Institute of Architects (AIA) reported the June ABI score was 51.6, down from a mark of 52.9 in May. This score reflects an increase in demand for design services (any score above 50 indicates an increase in billings). The new projects inquiry index was 62.6, up sharply from the reading of 59.1 the previous month.

Key ABI highlights and details on the construction industries remaining threats after the break...

Following the first negative downturn in ten months (what AIA Chief Economist, Kermit Baker, Phd, is hoping was just a "blip"), May's Architecture Billing Index (ABI) has bounced back from a score of 48.6 to 52.9. Any score above 50 indicates an increase in billings (aka an expansion in demand for architects' services).

Baker notes that "there is [still] a resounding sense of uncertainty in the marketplace from clients to investors and an overall lack of confidence in the general economy – that is continuing to act as a governor on the business development engine for architecture firms.” However, the scores, which revealed the most growth in the Northeast as well as in the multi-family residential and institutional sectors, are good signs for the design and construction industries.

More results of this month's ABI, after the break...

For the eight consecutive month, the Architecture Billings Index (ABI) is reflecting a steady upturn in design activity. As a leading economic indicator of construction activity, the ABI reflects the approximate nine to twelve month lag time between architecture billings and construction spending. Although the American Institute of Architects (AIA) reported the March ABI score was 51.9, down from a mark of 54.9 in February, this score still reflects an increase in demand for design services (any score above 50 indicates an increase in billings). In addition, the new projects inquiry index was 60.1, down from the reading of 64.8 the previous month.

“Business conditions in the construction industry have generally been improving over the last several months,” said AIA Chief Economist, Kermit Baker, PhD, Hon. AIA. “But as we have continued to report, the recovery has been uneven across the major construction sectors so it’s not a big surprise that there was some easing in the pace of growth in March compared to previous months.”

Key ABI highlights and details indicating higher employment rates for intern architects after the break...

An increasing demand for design services in the United States continues to strengthen the Architecture Billings Index (ABI). As a leading economic indicator of construction activity, the ABI reflects the approximate nine to twelve month lag time between architecture billings and construction spending. The American Institute of Architects (AIA) has reported the February ABI score as 54.9, up slightly from a mark of 54.2 in January. This score reflects a strong increase in demand for design services (any score above 50 indicates an increase in billings). In addition, the new projects inquiry index was 64.8, higher than the reading of 63.2 the previous month and its highest mark since January 2007.

“Conditions have been strengthening in all regions and construction sectors for the last several months,” said AIA Chief Economist, Kermit Baker, PhD, Hon. AIA. “Still, we also continue to hear a mix of business conditions in the marketplace as this hesitant recovery continues to unfold.”

Reflecting the strongest growth since November 2007, the January Architecture Billings Index (ABI) surged to a score of 54.2 - a sharp and welcomed increase from December’s 51.2* mark. Released by the American Institute of Architects (AIA), the ABI is a leading economic indicator of construction activity that reflects the approximate nine to twelve month lag time between architecture billings and construction spending. By remaining above 50, January’s score illustrates the six consecutive month of growth for the United State's design and construction industry. This trend doesn't seem to be going away any time soon, as the new projects inquiry index accelerated beyond last month's reading of 57.9 and reached a score of 63.2.

“We have been pointing in this direction for the last several months, but this is the strongest indication that there will be an upturn in construction activity in the coming months,” said AIA Chief Economist, Kermit Baker, PhD, Hon. AIA. “But as we continue to hear about overall improving economic conditions and that there are more inquiries for new design projects in the marketplace, a continued reservation by lending institutions to supply financing for construction projects is preventing a more widespread recovery in the industry.”

Review the ABI Highlights in greater detail, after the break...

Concluding 2012 with strong business conditions, the December Architecture Billings Index (ABI) marks five consecutive months of growth with a score of 52.0. Released by the American Institute of Architects (AIA), the ABI is a leading economic indicator of construction activity that reflects the approximate nine to twelve month lag time between architecture billings and construction spending. By remaining above 50, December’s score reflects an increase in demand for design services. However, growth is slightly slower than the previous month, whose mark at 53.2 brought the strongest business conditions since 2007. Additionally, the new projects inquiry index remains in positive territory with a score of 59.4, also down slightly from the 59.6 mark of November.

The numbers are in and the American Institute of Architects’ November Architecture Billings Index (ABI) has revealed positive business conditions for all building sectors for the fourth consecutive month.

As a leading economic indicator of construction activity, the ABI reflects the approximate nine to twelve month lag time between architecture billings and construction spending. Understanding this, the AIA is pleased to report that November has reached a five-year high with a score of 53.2, slightly up from 52.8 in October. Since August, the national billings index has continued to increased above 50.0 – the break-even point between contraction and growth – reflecting a steady rise in demand for design services. The West seems to be the only region in contraction, coming in at a score of 49.6.

Additionally, November also sees the Project Inquiry Index at 59.6, marking the 47th straight month in which inquiries into architectural services has been increasing.

“These are the strongest business conditions we have seen since the end of 2007 before the construction market collapse,” said AIA Chief Economist, Kermit Baker, PhD, Hon. AIA. “The real question now is if the federal budget situation gets cleared up which will likely lead to the green lighting of numerous projects currently on hold. If we do end up going off the ‘fiscal cliff’ then we can expect a significant setback for the entire design and construction industry.”

View the ABI highlights in greater detail, after the break…

In continuing our coverage of the Architecture Billings Index, we share this past month’s score of 48.7 While such a mark still falls in negative territory (any score under 50 indicates a decline in billings), July’s activity was a considerable jump from June’s meager 45.9. And, even better, July’s new projects inquiry index moved up almost two full points to 56.3. Regionally, the South is surprisingly leading the averages with 52.7, followed by the Midwest with 46.7, the West with 45.3, and lastly, the Northeast region capping out at 44.3. In terms of the sector breakdown, multi-family residential remains strong with 51.4 followed by commercial/industrial projects and institutional projects. AIA Chief Economist, Kermit Baker, PhD, Hon. AIA, explained, “Even though architecture firm billings nationally were down again in July, the downturn moderated substantially. As long as overall economic conditions continue to show improvement, modest declines should shift over to growth in design activity over the coming months.”

The June ABI has proven that we still have not been able to shake the weak activity of May - the score capped out at 45.9 from 45.8, marking the third month in negative territory. The market continues to show a drop in demand across all design services, in all regions. The poor conditions suggest upcoming weakness in spending on nonresidential construction projects, as each sector of construction shows negative growth commercial/industrial 46.9, institutional 46.0, and mixed practice 45.9. “The downturn in design activity that began in April and accelerated in May has continued into June, likely extending the weak market conditions we’ve seen in nonresidential building activity ,” said AIA Chief Economist, Kermit Baker, PhD, Hon. AIA. “While not all firms are experiencing negative conditions, a large share is still coping with a sluggish and erratic marketplace.”

The Architecture Billings Index (ABI) has clocked in at a positive 50.9 for January. Although the score brings the ABI into positive territories for the past three months, 50.9 is slightly over the positive measuring marker and actually, just under December’s mark of 51.0. Regional averages place the Midwest as the leading area with 53.7; followed by the South (51.6), Northeast (50.7), and West (45.6). AIA Chief Economist, Kermit Baker, PhD, Hon. AIA explained that even though the index is showing a similar upturn in design billings to the late 2010 and early 2011, firms are still having a hard time staying on their feet. “We still continue to hear about struggling firms and some continued uncertainly in the market, we expect that overall economic improvements in the design and construction sector to be modest in the coming months.”

We are happy to report another positive showing for the ABI this month as the index remained at 52.0 for the month of December. Prior to November, the volatile ABI showed the struggling and unstable conditions many practices were experiencing throughout 2011; yet, this month brings another bit of hope for the profession. “We saw nearly identical conditions in November and December of 2010 only to see momentum sputter and billings fall into negative territory as we moved through 2011, so it’s too early to be sure that we are in a full recovery mode,” said AIA Chief Economist, Kermit Baker, PhD, Hon. AIA. “Nevertheless, this is very good news for the design and construction industry and it’s entirely possible conditions will slowly continue to improve as the year progresses.” Regional breakdowns are as follows: Regional averages: South (54.2), Midwest (53.1), Northeast (52.6), West (45.1) and Multim-family residential led the sector index breakdown with 54.3. It was nice to finish the rocky year of 2011 with a consecutive positive index, and we’re optimistic for more improvement in 2012.

We have been covering the fluctuating Architecture Billing Index for several months, anxious to see steady improvement in our economy and our profession’s field. In the month of April, a survey was included in the Billings Index and the AIA recently released the findings. As John Schneidawind reported, almost two-thirds of the surveyed architects reported at least one stalled project due to lack of financing, despite record low interest rates.